Social Security retirement benefits provide a cadence of guaranteed income. But do clients know exactly how much of their Social Security benefit is taxed?

Social Security retirement benefits provide a cadence of guaranteed income. But do clients know exactly how much of their Social Security benefit is taxed?

The taxation of Social Security retirement benefits can be a source of great confusion for both taxpayers and even those within the financial services industry. Many mistakenly assume benefits are either entirely tax free or subject to an 85% tax rate. While some may not pay taxes on their benefits, those who do often are surprised to find the taxable portion is smaller than anticipated.

These insights can help clients understand how their Social Security retirement benefits may be taxed, which also can clarify when and how they should claim

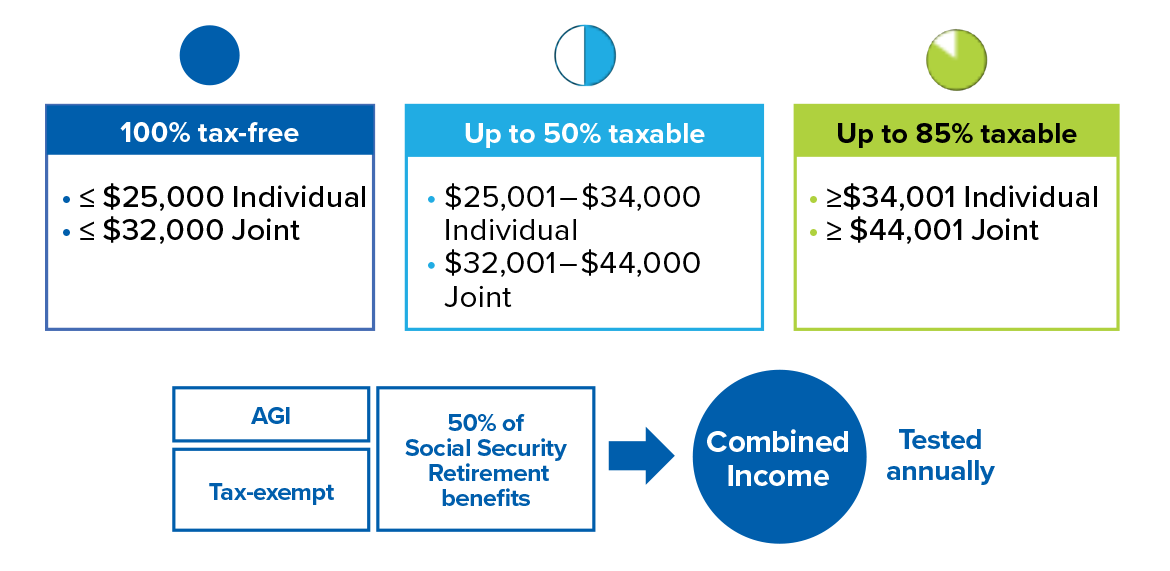

Social Security retirement benefit payments may be subject to federal income taxes, and the chart below outlines the taxation thresholds. If a client’s provisional income exceeds a threshold, then, up to that portion of their benefit is included in the client’s adjusted gross income (AGI). The maximum inclusion is 85%, leaving 15% free of federal income taxes.

It’s also important to note that these numbers are the maximum amounts that can be included in taxable income. The actual number could be less based on the three-part test, which we’ll cover below.

Source: Social Security Administration. “Publication 05-10035, Retirement Benefits.” January 2024. Accessed March 18, 2024.

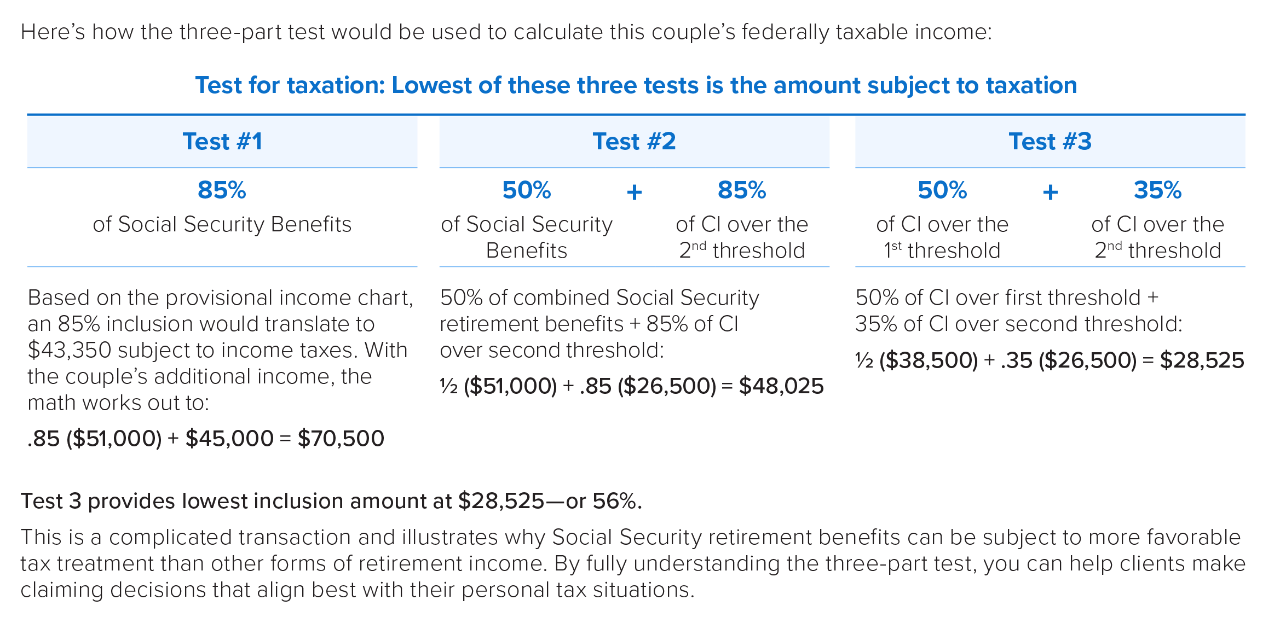

The three-part test uses additional client information to calculate his or her actual amount of taxable Social Security retirement benefits. As shown in the tables included here, the test calculates taxable income three ways: 85% of the total Social Security benefit, 50% of the total benefit plus 85% of a married couple’s combined income (CI) over the second threshold listed in the example to the left, or 50% of CI over the first threshold plus 35% of CI over the second threshold. Whichever value is lowest is the actual amount of a client’s Social Security retirement benefit subject to federal income tax.

To outline how this works in practice, imagine a married couple with a combined annual Social Security retirement benefit of $51,000 and $45,000 in additional income subject to federal income tax.

Here’s how the three-part test would be used to calculate this couple’s federally taxable income:

Test 3 provides lowest inclusion amount at $28,525—or 56%.

This is a complicated transaction and illustrates why Social Security retirement benefits can be subject to more favorable tax treatment than other forms of retirement income. By fully understanding the three-part test, you can help clients make claiming decisions that align best with their personal tax situations.

The decision to claim Social Security retirement benefits has multiple planning implications, and taxes will play a significant part. With partially tax-exempt income at the federal level, individuals may find that their MAGI is lower than anticipated, allowing them to take advantage of tax-planning opportunities that might be available with lower MAGI. An example is a Roth conversion. The conversion adds to ordinary income but could be an amount that does not exceed the current tax bracket. Taxpayers can manage their retirement-income tax obligations which may allow them to keep more of their income to maintain their desired retirement lifestyles. Remember that in retirement, taxes are paid by the retiree’s income, including distributions from savings and qualified accounts. If the retiree is required to take a larger distribution from his or her accounts to cover taxes, it can affect how long the portfolio assets will last. The sustainability of the portfolio potentially affects retirement lifestyle.

ACTIONS YOU CAN TAKE RIGHT NOW

For more information about retirement-planning, please contact our Retirement Strategies Group at RSG@PacificLife.com or (800) 722-2333, ext. 3939. PacificLife.com

This material is provided for informational purposes only and should not be construed as investment, tax, or legal advice. Information is based on current laws, which are subject to change at any time. Clients should consult with their accounting or tax professionals for guidance regarding their specific financial situations.

Pacific Life refers to Pacific Life Insurance Company and its subsidiary Pacific Life & Annuity Company. Insurance products can be issued in all states, except New York, by Pacific Life Insurance Company and in all states by Pacific Life & Annuity Company. Product/material availability and features may vary by state. Each insurance company is solely responsible for the financial obligations accruing under the products it issues.

The home office for Pacific Life & Annuity Company is located in Phoenix, Arizona. The home office for Pacific Life Insurance

Company is located in Omaha, Nebraska.

This material is educational and intended for an audience with financial services knowledge.

No bank guarantee • Not a deposit • May lose value

Not FDIC/NCUA insured • Not insured by any federal government agency

24-220

VLQ3428BG-2400

56/24 E627

Pacific Life, its affiliates, distributors, and respective representatives do not provide tax, accounting or legal advice. Any taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor or attorney.

Pacific Life is a product provider. It is not a fiduciary and therefore does not give advice or make recommendations regarding insurance or investment products.

Unless otherwise noted, all aforementioned money managers, their distributors, and affiliates are unaffiliated with Pacific Life and Pacific Select Distributors, LLC.

Insurance products and their guarantees, including optional benefits and any crediting rates, are backed by the financial strength and claims-paying ability of the issuing insurance company, but they do not protect the value of the variable investment options. Look to the strength of the insurance company with regard to such guarantees because these guarantees are not backed by the independent broker/dealers, insurance agencies, or their affiliates from which products are purchased. Neither these entities nor their representatives make any representation or assurance regarding the claims-paying ability of the issuing company.

Pacific Life refers to Pacific Life Insurance Company and its subsidiary Pacific Life & Annuity Company. Insurance products can be issued in all states, except New York, by Pacific Life Insurance Company and in all states by Pacific Life & Annuity Company. Product/material availability and features may vary by state. Each insurance company is solely responsible for the financial obligations accruing under the products it issues.

Variable insurance products are distributed by Pacific Select Distributors, LLC (member FINRA & SIPC), a subsidiary of Pacific Life Insurance Company and an affiliate of Pacific Life & Annuity Company.

The home office for Pacific Life & Annuity Company is located in Phoenix, Arizona. The home office for Pacific Life Insurance Company is located in Omaha, Nebraska.

No bank guarantee • Not a deposit • Not FDIC/NCUA insured • May lose value • Not insured by any federal government agency

For financial professional use only. Not for use with the public.